Tribunal judge Kevin Poole handed down the ruling in favour of HMRC last month at the First-Tier Tax Tribunals centre in Birmingham.

Biffa, Devon Waste Management and two Veolia UK companies all saw their appeals, which were launched separately but heard together, dismissed at the Tribunal hearing. Now another appeal is set to be lodged over the case by Biffa but neither Veolia nor Devon Waste have indicated what their next steps will be.

Fluff

The case relates to what is referred to as ‘fluff’, which, the Tribunal noted, generally consists of black bag waste. This is deposited at the base of where landfilled waste is buried, as well as up its sloping side and/or on top of the main body of landfilled waste.

This works as a type of buffer between the deposited waste and the lining material, which the court heard evidence to say can cost upwards of £1.6 million. A key consideration in laying this first layer, noted the Tribunal, is to reduce the risk of puncture to the “all-important liner”.

The three companies argued that as the waste was being ‘used’, it was not being deposited as waste and therefore not liable for landfill tax as outlined in the Finance Act of 1996, which defines what is a “taxable disposal” for the purposes of landfill tax.

HMRC argued that the material, despite its use, is still sent to landfill sites with the intention of staying there, and is thus classified as waste.

2008 ruling

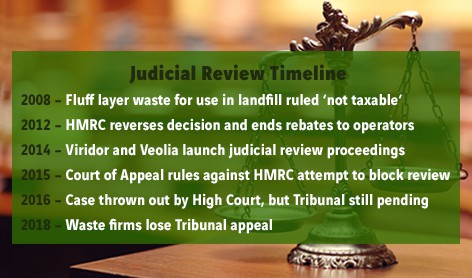

The issue dates back to 2008, when HMRC said it would not appeal against a ruling in which a court found in favour of Waste Recycling Group (WRG).

WRG had successfully argued that a landfill site operator, who had used various inert materials for building roads and for ‘daily cover’ on a landfill site, did not have the intention of discarding it as it had retained and used the material for its own purposes.

HMRC then issued a brief summarising the effect of the decision, explaining that material put to use on a landfill site was not taxable, giving “illustrative examples” of such use.

HMRC then invited claims for repayment of landfill tax which fell within such examples. This is when various waste companies put forward claims relating to landfill fluff, according to evidence presented to the High Court.

In mid-2009 HMRC decided that base and side fluff claims were in principle, well founded. According to the High Court ruling in 2016, HMRC made “substantial repayments in relation to base and side fluff”.

The tax authority however also claimed to have started receiving claims for ‘top fluff’ or ‘reverse fluff, according to court documents, which also said that HMRC could find no trace of the term ‘top fluff’ being used before the brief was issued.

HMRC then “suspected that the idea had been invented to generate tax repayments”, the court documents added. In June 2012, HMRC subsequently said in a brief it would not repay for ‘top fluff’.

In December 2013, HMRC went further and decided to stop repaying on base and side fluff as well, but said it would not seek to reclaim what it had already paid and issued a brief explaining this in 2014.

Judicial Review

After the waste management companies sought judicial review, Justice Nugee of the High Court threw out the case in2016 (see letsrecycle.com story).

He resolved that the base and side fluff claims were a “relatively early skirmish” in what had become “an all-out attack on the tax as a whole”. He suggested that had HMRC known at the outset the extent of the challenge, “the whole approach would have been different”.

As a result of the ruling HMRC were not required to issue rebates to the companies in this case, but appeal proceedings to determine whether the material used was or was not subject to landfill tax were put forward in a separate first-tier tax tribunal, in which a decision as handed down last month.

Ruling

In the first-tier tax tribunal, Judge Poole explained that when making his decision, he must consider if the person making the disposal does so “with the intention of discarding the material”.

In dismissing the appeal, he said: “In one sense, it is clear that the material is “used” to protect the lining system – indeed Ms Hall [HMRC’s representative] accepted this was the case.

“But that is not the end of the matter. It is clear that all the material was destined for landfill in any event, in the main body of landfilled waste if not as “fluff”.

Mr Poole added that common sense is often needed when reviewing what on a landfill site can be deemed as being landfilled, but said the court does “not consider the deposit in a landfill cell of black bag waste which is intended to remain there permanently to be one of those exceptions.”

Judge Poole concluded: “We therefore find that the deposits of fluff were all made by way of landfill”.

Reaction

Commenting on the Tribunal decision, a spokesman for Biffa said: “This is the latest instalment in a long-running saga and the company is going to appeal the decision.”

And the spokesman confirmed that the potential costs of the dispute had been allowed for before the company was listed on the Stock Exchange. He said: “The amount in dispute has already been paid in full, and at IPO in 2016 a structure was put in place to ensure that the exposure relating to the dispute was limited to pre-IPO shareholders. Therefore, and irrespective of the final outcome of the appeal, there will be no material impact on the business.”

A spokesman for Veolia said that the company’s legal department had no statement on the matter.

A comment has been requested from Devon Waste Management.

Register for free to comment