After a challenging 2020 for everyone from a personal and business perspective, it is good to look forward towards what can be achieved in the future. Although the next ten years will continue to bring huge challenges for the UK plastic recycling industry, there are also opportunities as the level of recycled content in products increases and there is a move to towards the circular economy.

In January 2021, the British Plastics Federation (BPF) released a Recycling Roadmap, which looks at what the UK could achieve by 2030, provided the right drivers are in place. Drastically reducing our reliance on exporting plastic waste and reducing plastics going to landfill to 1% over the next ten years is possible. There is a lot of positive progress that can be built upon but there needs to be significant investment to overcome some existing challenges, including much-needed growth in domestic mechanical and non-mechanical recycling capacity, as well as developing or expanding recycling systems for non-packaging plastic waste.

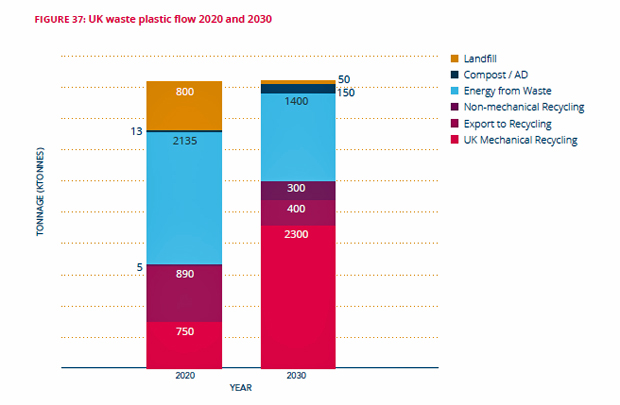

What could plastic recycling look like in 2030?

By looking at what it is possible to achieve within the next 10 years, the BPF has forecasted the end of life destinations for plastic in 2030. In this forecast, there is no reliance on low quality exports of plastic waste. The plastic waste that is exported is less than half of current figures and the material we export would be to achieve the best environmental outcome, in cases where there are no facilities to recycle this within the UK.

The other important change is more than tripling the amount of material mechanically recycled in the UK. This will help reduce reliance on exports, improve the traceability of waste, ensure there is recyclate available in the UK for manufacturers and provide jobs. The forecast has landfill becoming the end of life route for only 1% of material, recognising plastic is too valuable to end up there.

Another key change is in the level of material going to non-mechanical recycling facilities and this will be discussed in more detail later. With a drive to divert more plastic to recycling, plastic going to Energy from Waste (EFW) is expected to decrease to 30% (from over 45%).

What key changes are needed to achieve this?

The publication was developed by the BPF with input from a consultant as well as members of the BPF’s Recycling Group, which comprises 50 recyclers, to ensure that the projections it outlines are ambitious whilst also being achievable. However, this is not something that can be achieved without 16 key changes taking place, the report notes. The most essential requirement is for there to be significant investment in UK recycling infrastructure. This is something the BPF has been calling for over many years but it is even more critical now, with the need to rapidly create circular flows for more material and also to understand the ultimate end destination for the waste we are producing.

There is also currently the opportunity to provide this investment through the packaging tax if income from this was ringfenced for this purpose. The report estimates £1–1.3 billion is needed to build the required facilities in the UK just for the mechanical recycling sector.

“Household Waste Recycling Centres (HWRC) have a role to play”

The report recognises the role of Extended Producer Responsibility (EPR), which can provide a funding mechanism for some of the other key changes that are required. Improving collection systems is one of these. This is both in terms of consistent collections for households – with film recycling as part of the core set of material – but also the need to have easy-to-access collection for non-packaging (rigid) plastic materials. Household Waste Recycling Centres (HWRC) have a role to play here and by 2030 it would be expected all HWRC have containers for non-packaging plastics with facilities in the UK able to reprocess this material.

Communication also needs to have developed by 2030. This would not only include ‘yes/ no’ labels on packaging with information on where the material can be recycled but also more information for longer-life products. All long-life products should have information available online about how products can be repaired, upgraded or reused, as well as recycled. Householders would also be getting a minimum of one communication per year directly to their household, with information on how to recycle and motivation to increase their recycling.

End markets

End markets are vital to the success of recycling and by 2030 a mapping exercise will need to have taken place to identify for each plastic material the closed and open loop markets available, as well as manufacturing opportunities outside of the UK. This will help provide confidence for investment.

(article continues below)

(above: Location of pilot non-mechanical recycling plants or plants under construction)

Non-mechanical recycling

Non-mechanical recycling could be the end of life route for 7% of material in 2030. It includes recycling processes known under the umbrella term ‘chemical recycling’ as well as processes such as purification. This sector is set to see rapid growth, with lots of announcements taking place about collaborative projects being developed and facilities expected to be commissioned over the next few years. This may mean the forecast is on the conservative side but if this sector over-achieves this will only be a benefit, allowing more material to avoid ending up in landfill or an EFW facility.

The roadmap lists all the non-mechanical recycling companies the BPF is currently aware of with capacity in the UK or who are planning to establish capacity in the UK. It shows that significant investment is being made.

Where are we now?

The roadmap also paints a picture of where the plastic recycling industry was in 2020 and provides a central point for data on plastic recycling. It looks at ‘placed on the market’ (POM) data, waste arisings and recycling rates for all plastic sectors. Some sectors such as packaging have very good data available but in other areas it is limited such as end-of-life vehicles. When necessary and possible, estimates have been made to fill data gaps.

The overall picture across post-consumer plastic is an increase in recycling of over 150% since 2006 and a reduction in landfill of 70%.

Conclusion

The BPF believes that the next ten years will see considerable changes in plastic recycling. The forecast presented in the roadmap is achievable with the right drivers in place. The development of the plastic recycling sector, through the drivers set out in the report, is vital to creating a circular economy. There is currently a significant opportunity to create a turning point for the UK’s plastic recycling sector by investing money from the packaging tax in developing the UK’s recycling infrastructure. Improving collection systems so that as much plastic material as possible is collected for recycling and they are consistent across the country will reduce confusion for consumers, simplify communication and help meet growing demand for recycled plastic material. These steps could help the UK become a world leader in plastic recycling within a decade.

The BPF Recycling Roadmap is available to view and download for free at: bpf.co.uk/roadmap

Register for free to comment