This shows a considerable increase of almost 150,000 tonnes compared to the same period last year, suggesting that the UK market is continuing to grow in response to demand from energy from waste facilities in the likes of the Netherlands, Germany and Scandinavia.

However, the provisional figures are currently only available for the first two months of 2016 and some industry insiders believe the January and February tonnage could include some ‘overhang’ from the end of 2015.

This is because data is somewhat reliant on notifiers and consignees of material registering any recovered loads on a timely basis, and RDF can be stored for longer than a month after export before it is registered.

The overall tonnage exported throughout the whole of 2015 reached a new high – closing in on the 3 million tonnes mark (see letsrecycle.com story) – although the data also suggested that the level of year-on-year growth was starting to slow.

Nevertheless, the latest Agency TFS (transfrontier of shipment) figures do provide an indication that the huge export market growth since 2010 is far from flattening out entirely, despite previous predictions from the likes of the likes of consultancy Tolkvik that the market would peak at 2.5 million tonnes exported annually (see letsrecycle.com story).

And, a report earlier this year by consultancy Eunomia, which leads the RDF export industry group, claimed that that 2015 RDF exports could have reached as much as 3.3 million tonnes – a near 500,000 increase on 2014 (see letsrecycle.com story).

10 countries received RDF from the UK in January and February this year, with the largest takers of material remaining the Netherlands (280,000 tonnes), Germany (120,000) and Sweden (100,000).

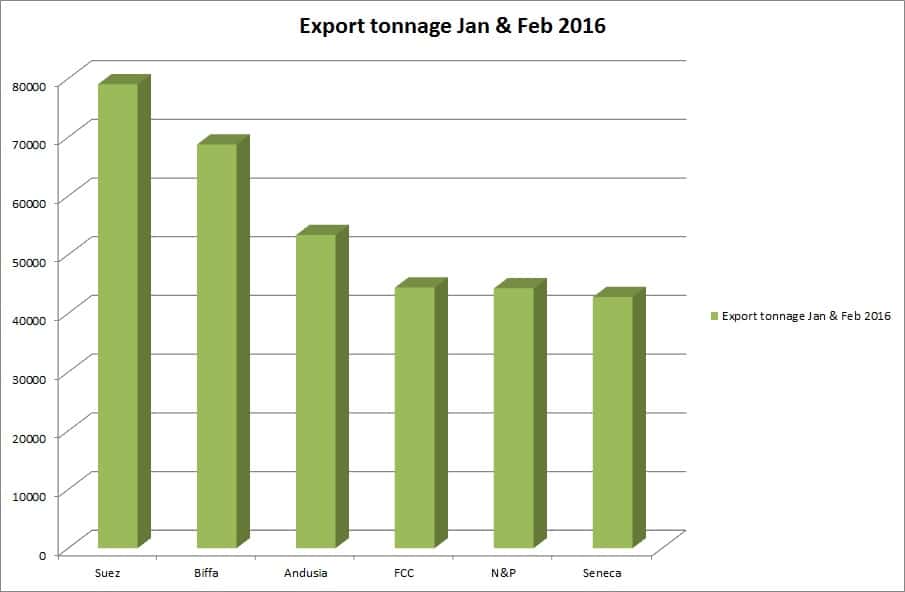

Meanwhile, among the 38 companies sending material abroad during this same period, the largest UK exporters were Suez (79,000 tonnes), Biffa (68,700) and Andusia Recovered Fuels (53,300).

Other notable entries include Veolia, which exported 2,730 tonnes during this period under its own name, and an additional 2,650 tonnes through its recent acquisition Boomeco.

Prices

Still, reports from UK operators and European EfW plants suggest that longer-term contracts are now being agreed with capacity filling up at on the continent and larger operators seeking to buy up contracts and consolidate the market.

With some EfW plants modifying prices in response, this has pushed operating costs and RDF gate fee prices up somewhat in the last couple of months, forcing some UK operators to look further afield for spare capacity as well as encouraging greater consolidation of the market.

Register for free to comment